1. The ASIC Report: A Snapshot of a Rapidly Expanding Industry

This week, the Australian Securities and Investments Commission (ASIC) released its much-anticipated report on non-bank lending, REP 820: Review of select non-bank lenders and private credit providers. The report shines a light on a sector that has grown rapidly in both visibility and volume, particularly as traditional credit conditions have tightened. ASIC’s review focused on 25 non-bank lenders, including private credit funds and mortgage-backed financiers, assessing lending practices, governance frameworks, and the extent to which borrowers understood loan terms and associated risks.

The key findings were mixed. On one hand, ASIC found that most participants operated with sound internal governance and disclosure practices. On the other, it identified areas of concern around borrower suitability assessments, fee transparency, and the adequacy of investor risk disclosures, particularly for complex products offered to wholesale and sophisticated investors. While there were no signs of systemic misconduct, the regulator expressed unease about the sector’s opacity, the lack of consistent reporting standards, and the rapid pace of growth.

In short, ASIC’s interest isn’t driven by scandal but by scale. Private credit has become too large, too fast, to ignore. The regulator is not just looking for wrongdoing, it’s assessing whether the existing oversight framework is still fit for purpose in a market that’s now moving billions in capital outside the traditional banking system. The attention, in other words, reflects the success of the sector as much as any perceived risk within it.

2. Why the Growth in Private Credit?

The growth of private credit can be traced to both sides of the market, investors seeking higher returns, and borrowers seeking flexibility. On the investor side, years of ultra-low interest rates compressed yields in traditional fixed-income markets. Institutional investors, from super funds to family offices, began allocating more to private credit, attracted by higher yields, shorter durations, and the ability to negotiate directly with borrowers. In a world where listed markets often feel overvalued and correlated, private debt also offers something rare, diversification.

From the borrower perspective, private credit fills the widening gap left by the banks. Post-Royal Commission reforms, tighter capital requirements, and risk-weighted lending standards have pushed banks further away from asset classes like construction funding, SME lending, and transitional property finance. For borrowers, private lenders can offer faster decisions, bespoke structures, and the ability to fund projects that sit just outside the banks’ increasingly narrow credit boxes. The trade-off, of course, is cost, interest rates and fees tend to be higher, but for many borrowers, access and speed matter more than price.

The result has been a boom in deal flow that banks wouldn’t, or couldn’t, touch. Many non-bank lenders have grown by capturing these “bank-rejected” opportunities, deals that are often sound but unconventional. For example, developers seeking residual stock loans, businesses in temporary turnaround, or borrowers with non-traditional income streams. In many ways, private credit isn’t displacing the banks, it’s absorbing the risk they no longer want to hold.

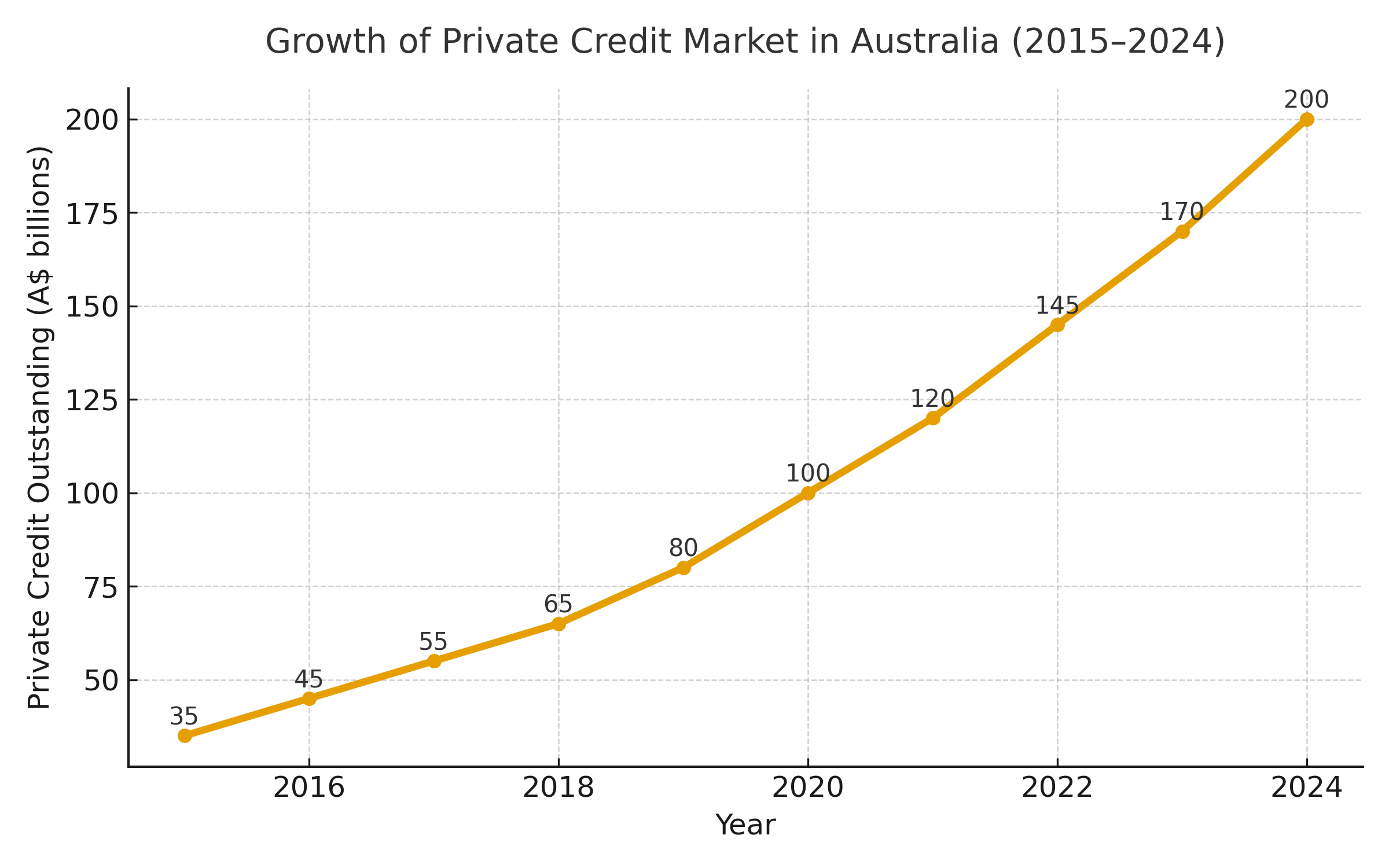

Australian Private Credit Growth (2015–2024):

The size of Australia’s private credit market has grown from approximately A$35 billion in 2015 to around A$200 billion in 2024.

3. Is This Just an Australian Phenomenon?

Far from it. The rise of private credit is a global trend, and Australia is arguably late to the party. In the United States, private credit has become a $2.1 trillion market, now larger than the entire U.S. high-yield bond sector. Europe has seen similar momentum, with institutional investors stepping in as banks pulled back post-GFC under Basel III and IV capital regimes. Even in Asia, traditionally dominated by relationship banking, private lenders are emerging as major participants in corporate and real estate finance.

In these markets, regulators have walked the same fine line ASIC now faces, encouraging capital formation while ensuring investor and borrower protection. In the U.S., for instance, the SEC has periodically raised concerns about valuation practices, leverage, and the opacity of private funds. Similarly, the Bank of England has flagged the potential for “liquidity mismatches” in private credit funds offering periodic redemptions. These are not new warnings, they’re the growing pains of a maturing asset class that now plays a critical role in global capital markets.

Historically, private credit markets have shown resilience through economic cycles, though not without issues. During the COVID-19 downturn, some funds faced redemption pressure and valuation uncertainty, but overall default rates remained lower than expected. The global experience suggests that while private credit introduces new risks, it also provides stability and liquidity to borrowers during periods when traditional banks retreat. That duality, risk and resilience, is what makes it both attractive and worthy of regulatory attention.

4. What Comes Next

The ASIC report doesn’t signal a crackdown, it signals a conversation. Regulators are trying to understand how to balance innovation and investor protection as Australia’s private credit market matures. We can expect more scrutiny around disclosure standards, governance practices, and the use of “wholesale investor” exemptions. Larger lenders may face pressure to adopt more consistent reporting frameworks, particularly as institutional investors continue to enter the space.

For borrowers and investors alike, this is not a reason for alarm, it’s a sign that private credit has become a meaningful and enduring part of the Australian financial landscape. As the report itself notes, private lenders are providing essential funding for businesses and projects that might otherwise stall. Regulation, if done well, could ultimately legitimise and strengthen the industry by improving transparency and investor confidence.

Globally, private credit has proven its capacity to operate responsibly and deliver strong, risk-adjusted returns. Australia’s challenge, and opportunity, is to scale that success within a regulatory environment that protects investors without stifling innovation. If history is any guide, the sector will continue to grow, adapt, and professionalise. And as ASIC looks more closely, it’s not because the industry is failing, it’s because it’s finally arrived.