The cash rate is expected to rise in the coming months. Mortgage rates, however, have been fluctuating since the beginning of the year and are more likely to continue fluctuating until the cash rate officially rises.

The four largest lenders ANZ and NAB have increased fixed rates for the sixth and seventh time in the last six months, respectively.

NAB and ANZ increased fixed interest rates on owner-occupier loans by up to 0.4 percentage points recently, a move aimed at reining in spiralling borrowing costs. Interest on one-year fixed rates has been reduced to 2.99 per cent for both.

Variable mortgage rates, on the other hand, have decreased across the board. Around 35 lenders now offered variable rates below 2 per cent, a report by RateCity stated. Variable mortgage rates have been reduced in tandem with the huge increase in fixed-rate mortgage offerings, as three- and five-year bond yields continue to surge.

Property buyers are receiving greater discounts from sellers and lenders are offering lower variable loan rates as national clearance rates fall below 70 per cent for the fourth consecutive week since March 2022, according to market analysis.

Over 70 lenders are giving headline variable rates of less than 2 per cent and additional incentives, such as new rounds of cashback guarantees, in an effort to attract new borrowers or entice existing borrowers to transfer.

Why are mortgage rates changing?

Fixed-rate mortgage rates are influenced by the bond market, which is where banks, corporations, and governments borrow money. Bond yields are rising sharply, boosting fixed-term borrowing costs, which are passed on to borrowers.

Between March 2020 and May 2021, the number of fixed-term loans climbed by more than 50 per cent. According to the Reserve Bank of Australia, they account for approximately 30 per cent of the total outstanding mortgage loan value.

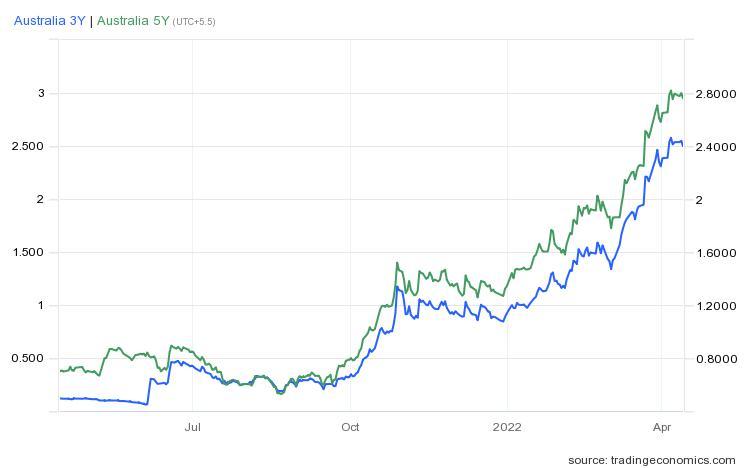

The steep increase in fixed rates is a result of rising three- and five-year bond yields, as global interest rate traders anticipated that central banks would begin an aggressive rate-raising cycle to combat growing inflation.

Image: A comparison between 3 and 5-year bond yield growth over the past year.

As per the latest sources, now that mortgage holders are locked in at a fixed rate, lenders are refocusing their efforts on variable rates. Variable rates are seen heading down due to this but this change will only be temporary. Lenders are also providing cashback packages up to $5,000 depending upon the loan size for first-time homebuyers as well.

CBA cut its lowest variable rate to 2.19 per cent last week to match NAB and ANZ. At 2.09 per cent, Westpac has the lowest rate. NAB demands a 20% minimum deposit. The other banks require a 30 per cent deposit.

Other lenders, including HSBC, ME Bank, and Citi, have lowered their interest rates on owner-occupier loans to less than 2 per cent.

Lenders are aiming to revitalise refinancing, which has fallen around 20 per cent – or almost $3.5 billion – since August 2021’s peak, by increasing incentives for borrowers to transfer to cheaper variable rates.

The ASX publishes data illustrating an implied yield curve based on futures market projections of the expected RBA cash rate in the near term. At the end of March 2022, the data gathered by researchers indicated an estimated cash rate of 1.00 per cent in September 2022 and more than 2.00 per cent in March the following year. From the present rate of 0.10 per cent, this implies that the interest paid on many loans may nearly double in a year.